The community bank is dying; some might argue it is already dead. The question is – why?

A large section of the industry, and those familiar with it, would hang a heavy burden of blame on the passage of Dodd-Frank in July 2010, which was widely heralded as the salvation of the banking system.

Since the law’s enactment, 1,341 banks have “disappeared,” according to a report from The Wall Street Journal. During the same period, only two new banks have been chartered. The regulations levied against banks as stipulated by Dodd-Frank have had the biggest impact on smaller banks, because, frankly, they struggle to afford compliance, which includes the cost to cover the additional staff needed to handle the newer, more strict standards for loan documentation.

In a survey conducted by George Mason University’s Mercatus Center, in which more than 200 banks across 41 states responded, the overwhelming response in regards to Dodd-Frank has been concern.

Maybe It’s Not All Dodd-Frank

Ninety percent of survey respondents claimed that since 2010, compliance costs have increased, and for 83 percent, the increase has been more than 5 percent. To handle the new compliance load, responding banks admitted to hiring 50 percent more compliance officer, specifically to deal with Dodd-Frank. However, overall industry employment has only increased 5 percent, keeping levels below pre-crisis benchmarks.

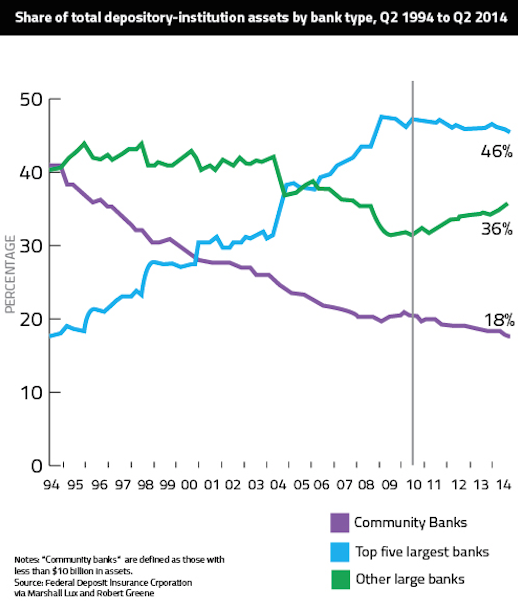

But while Dodd-Frank remains an easy scapegoat for the fading community banking system, the truth is that small banks have been consistently losing ground since 1985, as a result of the savings and loan crisis. In 1994, community banks handled 40 percent of deposits, and today that number has fallen to only 18 percent, JD Supra recently reported. As the graph below shows, the drop has been consistent.

With less business, smaller banks have struggled to maintain their community presence. As an act of survival, the popular option has been to merge with larger, less locally involved institutions.

A New Kind of Community Bank

Evan Tomaskovic, a partner at the New York-based Carl Marks Advisory Group, wrote in American Banker that while a cursory evaluation of the today’s banking landscape would seem positive – communities continue to be serviced by a bank, in the end – the side effects could be overall damaging.

“A startling negative side effect of this consolidation will be the loss of the true meaning of the word ‘community’ in community banking,” he explained. “Although the days of George Bailey may be long gone, the idea of a true community bank is still valued – one that is led by individuals who live in the area, have an ear to the ground, and know and care about their neighbors’ well-being – but it’s not likely to last as the consolidation movement gathers steam.”

In his article, Tomaskovic said that the acquirers of small banks are “likely to replace or eliminate the board and management of the target,” and in effect remove the community aspect of the community bank. “It comes down to cost synergies and redundancy.” Larger banks will look to see how smaller, local banks can add benefit to their regional structure, which, he warns, will mean stripping the existing executive hierarchy.