One thing about today’s housing market is that demand isn’t the problem.

Americans are continuing to move out on their own, grow their families and even choose to live independently for longer. While mortgage rates and inventory influence the direction of any market, household formation is at the forefront of the conversation. Recent data from both Realtor.com and the National Association of REALTORS® shows that household growth is steady but supply is still catching up.

NAR reports that household formation isn’t being driven by just one generation. Between 2023 and 2024, the largest increases in the number of households came from older Americans, particularly those ages 65 and older. However, at the same time, since 2019, household growth among adults ages 35-44 has also been strong, reflecting continued family formation and life-stage changes, according to NAR.

Realtor.com reports that approximately 1.4 million households were formed in 2025, while 1.36 million homes were started. During the same year, new construction fell short of household formation, widening the U.S. housing gap to an estimated 4.03 million homes.

That gap didn’t appear overnight. Realtor.com’s data shows that the U.S. has been underbuilding since at least 2012, creating a shortage that has only deepened over time. In 2012, the housing gap was estimated at just 1.5 million homes. By 2019, it had more than doubled to 3.84 million, before climbing in 2025. Even in years where construction activity improves, the housing market is still recovering from more than a decade of undersupply.

The difference between new households and new construction was only about 50,000 units in 2025. The homeowner vacancy rate fell to a historic low of 0.7% in Q2 2023. While it has since edged up to 1.2% by Q4 2025, it remains well below long-term norms.

Single-family starts declined from just over one million in 2024 to roughly 940,000 in 2025. Meanwhile, multifamily starts increased from 354,000 to 415,000, helping support rental supply more than ownership supply.

As a result, rental conditions have normalized faster than for-sale housing. Rental vacancy has recovered more than homeowner vacancy and is now back in line with its pre-pandemic range of roughly 7%, while the for-sale market remains far tighter by comparison.

During the pandemic and into 2024, new homes made up an elevated share of total inventory as existing homeowners stayed put longer. That trend continued into 2025. Even as their share of total inventory slipped, the number of new homes for sale was still rising 7% to 8% year over year in the first half of 2025, before cooling in November and falling 3.5% below the prior year’s level by December.

In 2025, new homes accounted for nearly 15% of all homes sold, the highest share since 2005.

Another key figure shaping today’s market is the estimated 1.8 million “missing” households among Gen Z and millennials. These are individuals who, under more typical housing conditions, likely would have formed their own households, but instead delayed due to affordability constraints and limited inventory. NAR data has supported this trend, showing that the median age of first-time homebuyers reached 40 in 2025.

Realtor.com notes that younger adults are forming households at lower rates than in previous decades, not because the desire isn’t there, but because financial barriers are getting in the way. Many are staying with family longer or living with roommates as they wait for a more accessible entry point into the market.

In 2025, the income required to purchase a median-priced starter home reached about $86,000. At the same time, a typical down payment of around $30,400 could take approximately seven years to save.

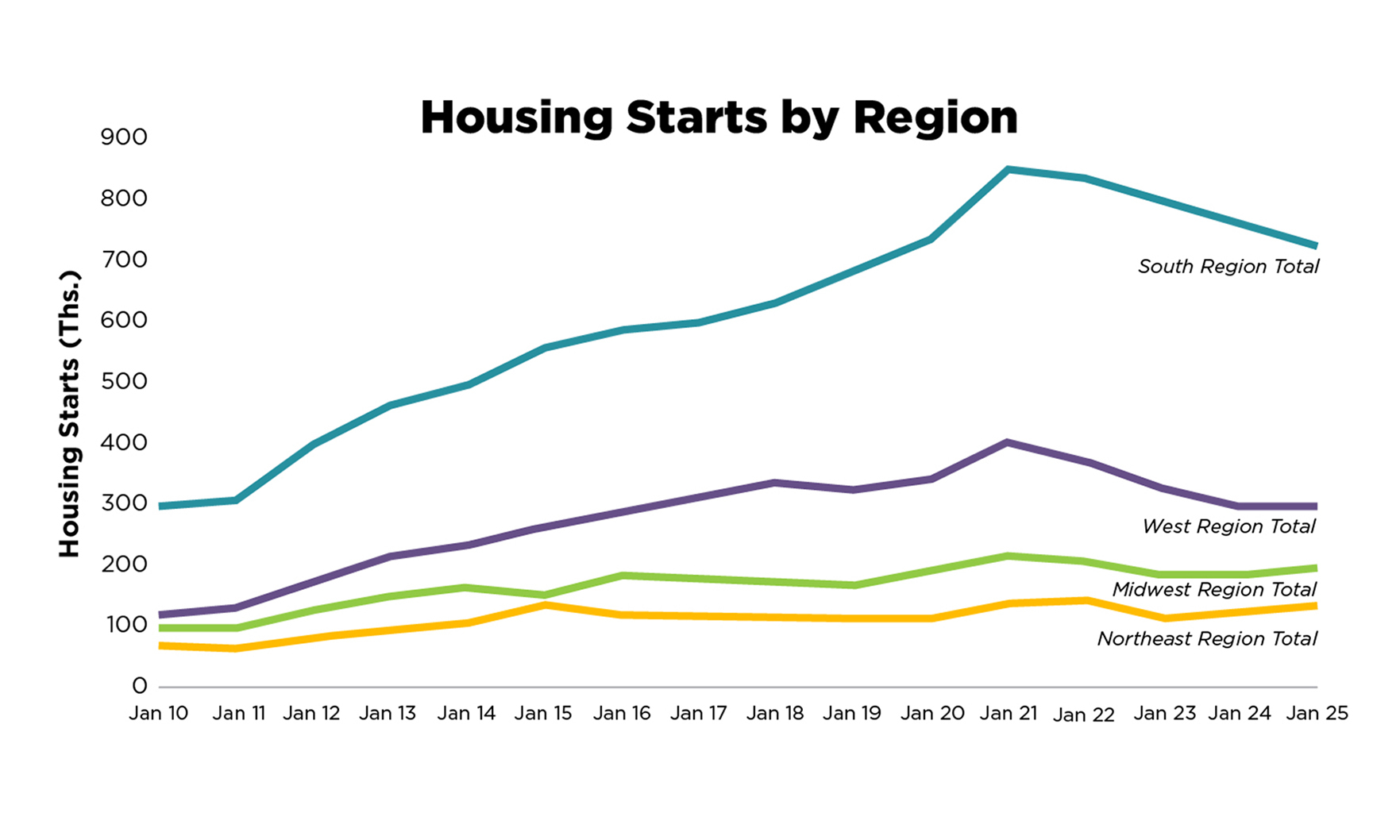

Regionally, the housing shortage varies, but it’s widespread. Realtor.com found that the South accounts for the largest share of the housing gap, at about 1.62 million homes. The West has the smallest gap, at roughly 660,000 homes.

However, the Northeast and Midwest emerge as the most undersupplied regions, meaning they have not built enough housing to keep pace with demand over time.

With household formation continuing across age groups and the housing deficit still in the millions, supply remains the market’s biggest constraint.