Despite recent improvements, there remain considerable uncertainties for consumers when it comes to housing and the economy.

Everywhere you look, nowadays, there seems to be a new study or report proclaiming good news about both housing and the greater economy. Are such reports, though, missing the larger narrative?

Don’t get us wrong, we’re hardly ones to contradict good news; after all, pending sales hitting their highest mark since June 2013 and the best job growth numbers in years are certainly things to celebrate.

That said, however, there remain worrying economic trends in terms of inequality, savings and wages (especially among Millennials), all of which continue to produce skepticism and uncertainty in consumers.

And that is why Fannie Mae’s National Housing Survey remains so critical. A detailed examination of the country’s economic sentiment, Fannie’s survey asks American consumers a wide range of questions about both housing and the economy, and has long offered a more nuanced take to the post-recession landscape than any one report or statistic.

So with that in mind, here are five of the most notable findings in Fannie’s latest survey:

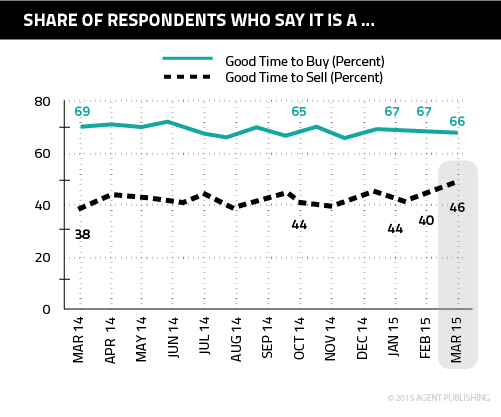

1. Consumers who say it is a good time to buy a house fell slightly, while those who say it is a good time to sell rose to 46 percent, which is a new survey high; many agents have told us that we’re now in a seller’s market, and consumers now seem privy to that knowledge.

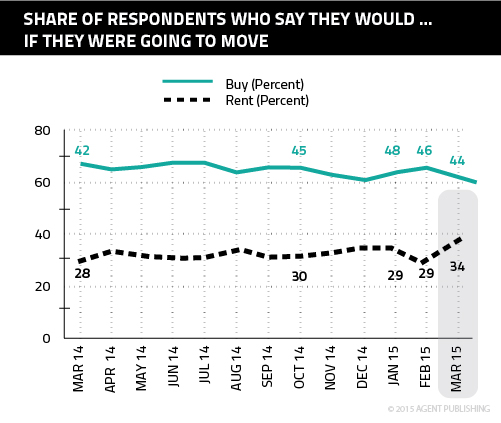

2. The share of consumers who say they would buy if they were going to move fell 5 percentage points to 60 percent – that’s a new survey low, and the share who would rent rose to 34 percent; perhaps the soaring home prices of the last two years are impacting how consumers view housing?

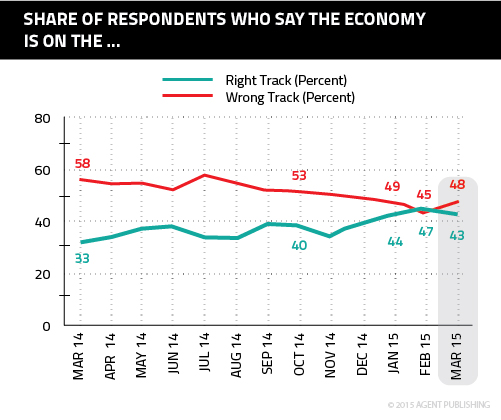

3. The share of respondents who say the economy is on the right track decreased by 4 percentage points to 43 percent, while those who say the economy is on the wrong track rose by 3 percentage points to 48 percent; notice how, after crossing paths briefly in February, the more consumers once again view the economy negatively.

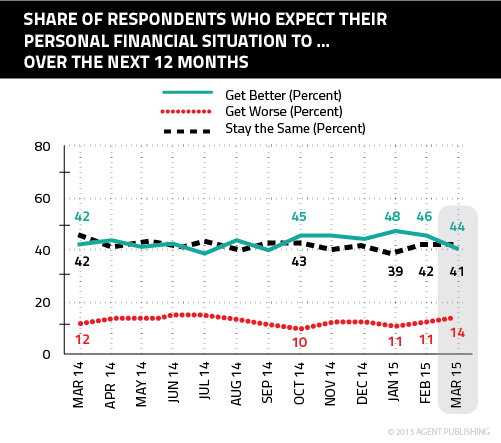

4. The percentage of respondents who expect their personal financial situation to get better over the next 12 months fell to 41 percent; as with our previous graph, we again see that optimism has fallen in favor.

5. Finally, the share of respondents who say their household income is significantly higher than it was 12 months ago fell 2 percentage points to 22 percent; meanwhile, as our graph below demonstrates, the share of respondents who say their household expenses are significantly higher than they were 12 months ago rose by 4 percentage points back to 35 percent – meaning that more than a third of consumers are unlikely to consider buying a home any time soon.

I pretty much agree with your findings.