Here’s what is known about Millennials: they aren’t buying homes, except that maybe some of them are buying homes. They definitely want to buy homes, but they don’t want to be tied down by a home. They understand the financial benefit of homeownership, but a lot them also regret the purchase and wonder if they can afford it.

Trying to get inside the minds of the 18-to-34-year-old generation has become something of a cottage industry for researchers and media members, and their seemingly infinite attempts to explain the group’s habits and desires are often contradictory. While there has been much panic over the generation’s consumption trends and what they could mean for different industries, it turns out that all the worrying about Millennials may have been premature.

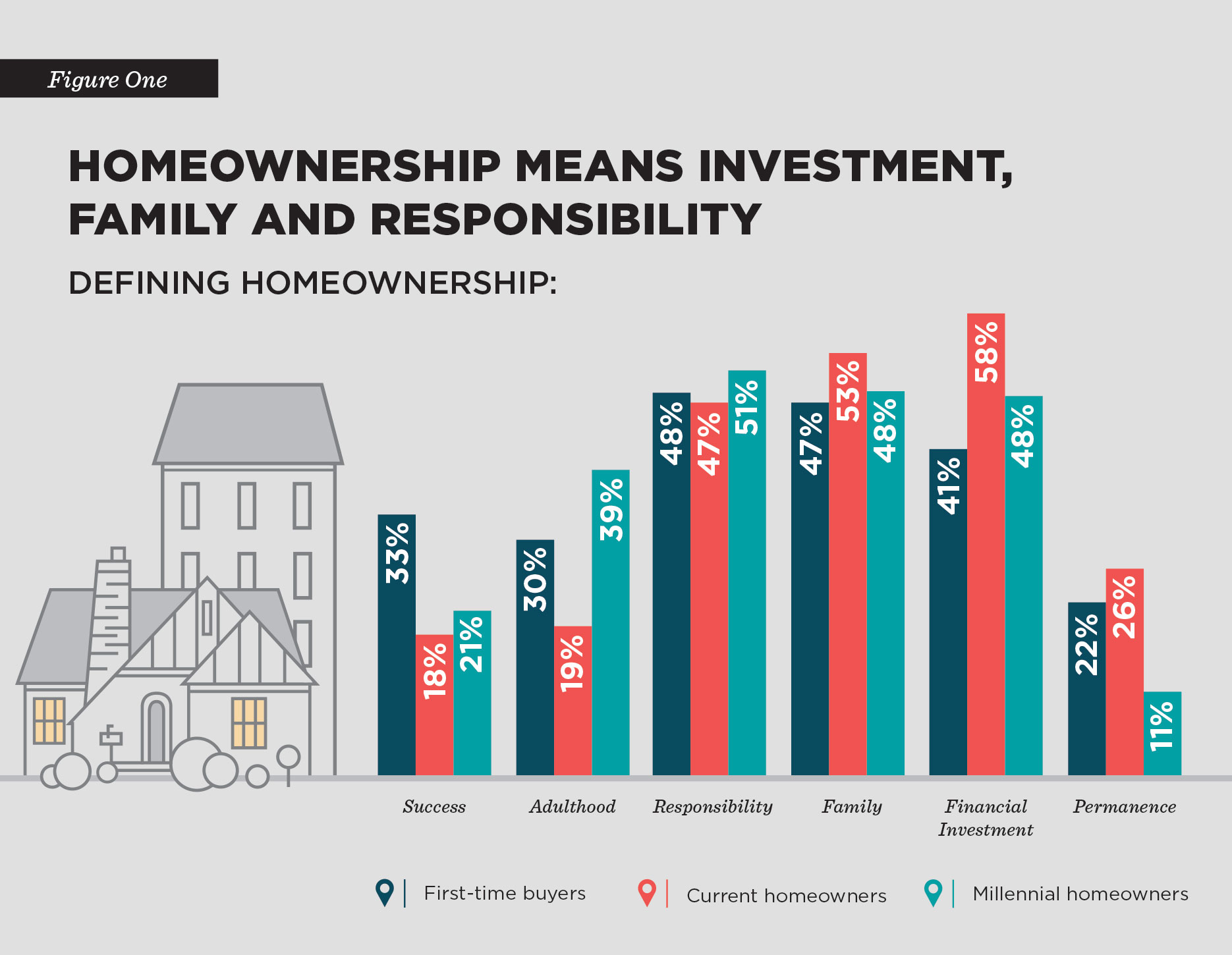

After wading through much of the surveys and research on Millennials’ homebuying habits, two facts help illustrate their views on homeownership and their current place in the housing market: Millennials were disproportionately effected by the Great Recession and housing market crash, and their views on homeownership and its place in the American Dream haven’t changed all that much.

Economic factors

It is true that Millennials own fewer homes and make up a smaller share of the homeowner population than previous generations of young people. The homeownership rate for the under-35 age group fell from 43 percent in 2005 to 31 percent in 2015, a historic low, according a 2017 study from Harvard University’s Joint Center for Housing Studies.

Much of the focus on Millennial homebuying has focused on their traits and habits, which are hard to define when describing what is now the largest generation in America. There are, however, financial indicators that show exactly why Millennials have been slow to enter the housing market.

For one, the Great Recession had a tremendous impact on Millennials and their ability to buy homes. Wages for Millennials have been stagnant, while costs like rent are taking up larger chunks of young people’s household pay, in turn keeping them from saving for a home. Similarly, higher education costs have doubled the rate of inflation, and Millennials are saddled with more student loan debt than any previous generation.

The housing market collapse also had a devastating effect on Millennials: their 16 percent decline in homeownership was the greatest dip of any demographic during the market collapse by far, according to a Fannie Mae study.

More than anything, Millennials aren’t buying homes for financial reasons. It doesn’t help that the age group prefers living in urban centers with expensive housing, but even that clues us in to what is keeping them from owning. Millennial homeownership rates are about 5 percent higher in cities where house prices are 20 percent below the national median average than in more expensive places, according to the Harvard study,

“The evidence suggests, however, that homeownership decisions by younger households have much more to do with affordability than location and lifestyle preferences,” the study reads. “Homeownership rates for the under-35 age group are in fact generally higher in metro areas where house prices are relatively low.”

Getting a late start

As Millennials age into their 30s and move beyond the effects of the recession and market collapse, it turns out their housing preferences are similar to other generations’. Survey after survey shows that Millennials want to buy homes, and now they are seemingly acting on that desire: the age group accounted for 34 percent of all homes bought in 2016, the largest share of any generation.

“If there’s one thing to take away from our report this year, it’s that forward-thinking Millennials are buying homes – and they’re happy with their choice,” D. Steve Boland, Bank of America consumer lending executive, said in this year’s Homebuyer Insights Report. “Clearly, the Millennial generation is coming of age and realizing it might not make sense to wait anymore to purchase their first home.”

Millennials buy the least expensive homes of any demographic, with a median home price of $205,000, according to the National Association of Realtors. They also purchase the smallest homes (median size: 1,800 square feet) and the oldest homes (median year built: 1984), suggesting that they recognize the benefits of owning before they are financially able to own their “dream home.”

In fact, 68 percent of Millennials surveyed in Bank of America’s report said their current home is a stepping stone towards the home they want to end up in. That suggests that Millennials plan to own more than one home throughout their lifetime, which is another good sign for the housing market.

“The overwhelming majority of Millennial homeowners say their current home is a ‘stepping stone’ to their forever home,” Boland said. “This growing group of Millennials is seeing the value of getting into a home.”