Mark Fleming, the chief economist at First American

Today, the Federal Reserve has its September meeting, where it could potentially decide to increase interest rates for the first time since 2008. The CME FedWatch Tool measures the market’s expectation of Fed target rates. Currently, the market-estimated probability of a 0.25 percent rate increase on September 17 is almost 80 percent.

Generally, it seems more likely than not that the Fed will increase rates, so its timely to ask, will a rate increase cause a collapse in the housing market as it forces up mortgage rates?

One argument is that rising interest rates cause affordability to decline, which is true. Many contend that declining affordability leads to a reduction in demand, which is not necessarily true, and that a reduction in demand means house prices will fall, which is not necessarily true either. People may adjust how much housing they demand, rather than drop out of the market all together. Of course, marginal borrowers may truly be priced out of the market, but it’s not clear that this reduction in demand would be significant enough to trigger falling prices. A slow down in the pace of price appreciation is a much more likely outcome.

Yet, I have argued here, as others have, that rising rates don’t necessarily cause a negative demand shock and falling home prices. When the Fed raises interest rates, it’s because the Fed believes that the economy is strong enough to adjust and has the potential to begin overheating (that’s what inflation measures). A stronger economy, more or better jobs, rising wages, increased confidence – these factors all increase demand for housing. In other words, rising rates are indicative of increased home sales and upward pressure on prices.

So, what scenario plays out if the Fed raises rates? Does reduced affordability win, or the better economy? Alas, we only observe the net effect of the two, but using our proprietary model of U.S. housing market existing-home sales demand and house prices, we can “ask” exactly what the net effect might be. In this case, what happens to existing-home sales and house prices when the Fed increases interest rates later this week by 0.25 percent and that causes a permanent upward shift in mortgage rates by the same amount?

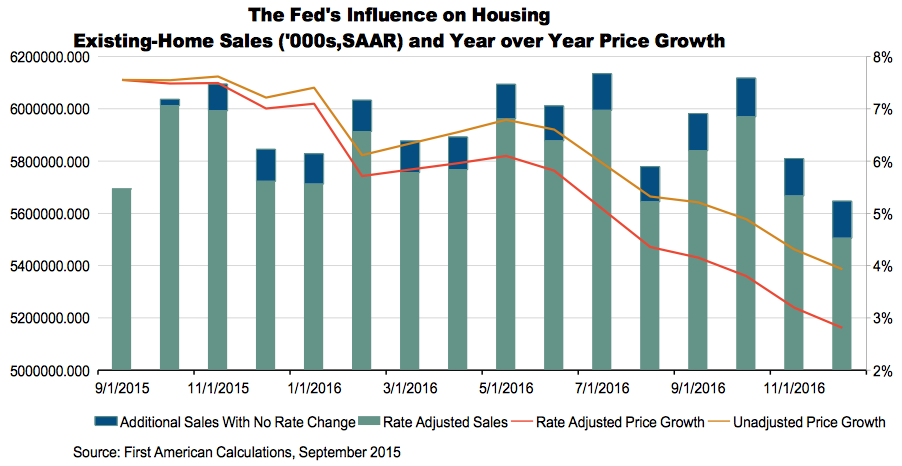

In the two figures below, we show the hypothetical result of a 0.25 percent increase to the 30-year fixed-rate mortgage rate this month caused by a Fed rate increase this week, and how that may influence the amount of existing-home sales demand and house prices through the end of 2016.

The first figure shows home sales and price changes, both with and without the rate increase:

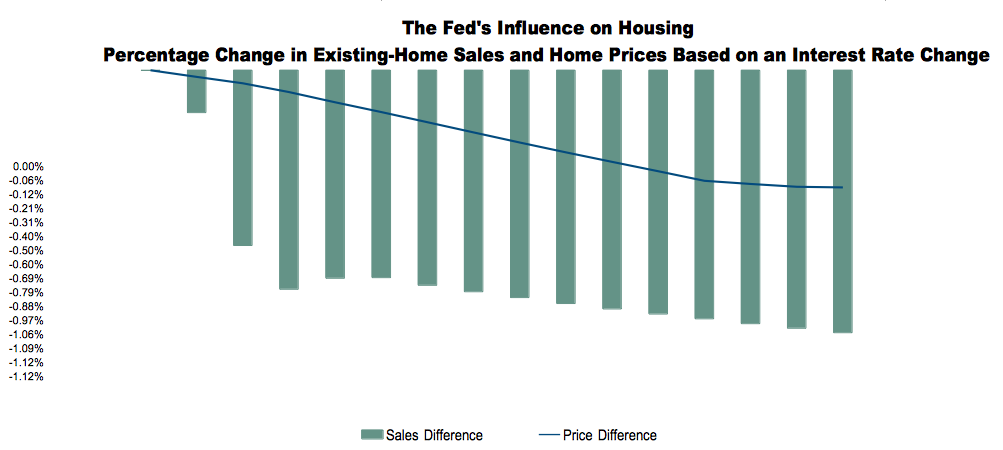

The second figure shows explicitly the differences between the two scenarios:

House price appreciation, on a year-over-year basis, does slow down, but only by 1 percent more than it is expected to slow down anyway. Existing-home sales also slow down, by about 2.5 percent on annualized and seasonally adjusted basis by the end of the time horizon. That turns out to be a hypothetical decline of less than 150,000 sales a year.

Of course, we cannot be sure exactly how mortgage rates and the housing market will respond to a Fed rate increase. But, we can say with some certainty that the Fed will eventually raise rates. When it does, the housing market isn’t doomed to fail, but rather adjust to the reality of interest rates that are reflective of a strengthening economy and certainly more traditional financial conditions. Is the housing market doomed? No, but the housing market will modestly adjust to a Fed rate increase.

Mark Fleming is the chief economist at First American. He was formerly the chief economist at CoreLogic and an economic with Fannie Mae, and has published research in the American Journal of Agricultural Economics and Geographic Information Sciences. He is a frequent source for national news outlets and industry trade publications, such as The Wall Street Journal, New York Times, and Housing Wire, and is a regular guest on news channels such as CBS, CNBC, Fox Business News, and NPR.