By Claire Easley

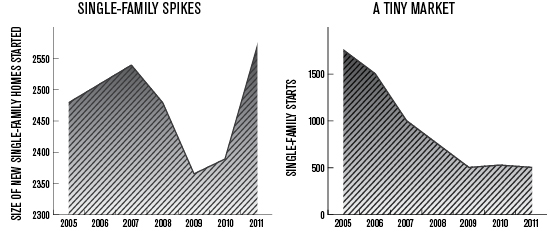

As the housing market entered its steep decline during the latter part of the past decade, it took home sizes with it. While there was much to bemoan about the state of the industry, among designers and architects it seemed the one bright spot was what appeared to be the demise of the McMansion and an increased focus on efficient functionality. Between 2007 and 2010, the average size of a new, single-family home in the U.S. fell from 2,504 square feet to 2,381 square feet, according to U.S. Census data. It was the rise of smaller and smarter.

Or was it?

“For all these years, the trend was going [down], and then in 2011, it reversed,” says Rose Quint, assistant vice president of survey research at the National Association of Home Builders. “Everything we had heard from builders, from architects, from consumers … was all pointing to a smaller home. But then in 2011 that all seemed to go under the bus.”

Between 2010 and 2011, average new, single-family home sizes spiked to 2,522 square feet—larger than during the height of the boom, leaving the industry wondering whether smaller homes were ever truly in vogue or if they were simply a necessity due to tight credit, high unemployment and a lack of equity.

In an effort to find the answer, Builder analyzed data from 12 metro areas around the country — including Boston; Chicago; Orlando, Fla.; Philadelphia; Phoenix; Raleigh, N.C.; Salt Lake City; Seattle; and Washington, D.C. — looking at a range of data from home sizes to financing to unemployment and others, between 2005 and 2011. (Most regional data was provided by Hanley Wood Market Intelligence, a division of Hanley Wood, Builder’s parent company.)

Among the 12 MSAs analyzed, all but one saw average home sizes fall over the six-year period, and all saw a decline in price per square foot.

The one metro area that bucked the trend for shrinking sizes was Philadelphia, which saw a small uptick in home sizes between the years, moving up 0.61 percent to an average of 1,829 square feet among all housing types. The market also saw the smallest decline in price per square foot, which dropped only 1.4 percent. Much of that trend has to do with who is buying the homes, says Greg Lingo, president at Media, Pa.–based Cornell Homes. “We’re generally seeing over the last year that people buying single-family homes are much more qualified in the ability to get a mortgage. It’s truly a move-up buyer.”

But even at the other end of the market, Lingo says Philadelphia buyers are turning to attached townhomes in order to get more space at a price they can afford. “It’s not a preference for the long term, but with family changes and economic changes, it’s a better value for the square footage,” he says. “Nobody wants a smaller home, necessarily. It’s really what they need. In this economy, people are weighing wants versus needs.”

Among the 12 MSAs analyzed, all but one saw average home sizes fall over the six-year period, and all saw a decline in price per square foot.

Indeed, the average percent financed among new-home sales in the area fell from 81 percent in 2005 to 73 percent in 2011. Mortgage financing fell by 88 percent over the same period, a trend likely related to the metro areas’ unemployment rate, which stood at 9.5 at the end of 2011—the highest of the 13 areas studied, according to the U.S. Bureau of Labor Statistics. During the same six-year period, average price per square foot costs fell by 34.6 percent.

However, just as tight credit contributed to the precipitous fall in home sizes during the housing market’s decline, it may once again be lack of credit driving the trend — this time skewing sizes by keeping first-time buyers out of the market. “We see a trend emerging now where lower price points are coming back,” Hansen says. “People are calling and asking about new construction under $200,000. … I do anticipate that smaller homes and lower price points will become more a part of our mix at the end of the year.”

That top-heavy recovery is also what Quint says is behind the national numbers. “The people who were able to buy a home last year had super good credit, super good savings, super good employment — otherwise you would not be able to get a loan. New single-family home starts were 75 percent lower [in 2011 compared to 2005], so it’s such a tiny market now that this small group of buyers’ preferences are dominating the market.”

COPYRIGHT 2012 HANLEY WOOD LLC

REPRINTED WITH PERMISSION FROM BUILDER MAGAZINE