Nearly 957,000 renters in the Chicagoland housing market struggle with the cost of housing, according to a new report from the Joint Center of Housing Studies at Harvard University.

Titled “America’s Rental Housing,” the center’s report examined how low inventory and high rents have placed millions of households in a bind.

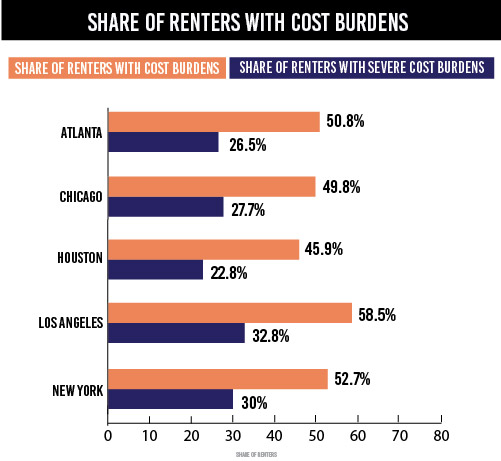

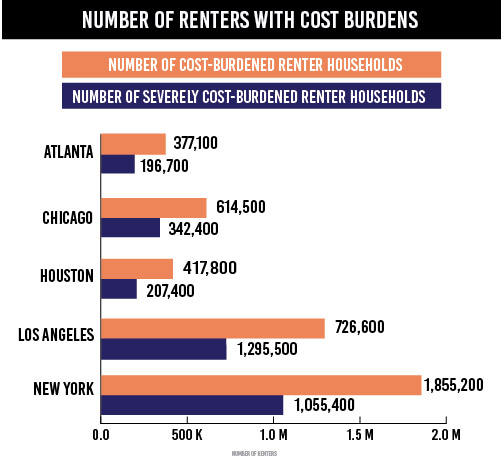

Here in Chicagoland, 49.8 percent of renters (or 614,500) face cost burdens, meaning they spend more than 30 percent of their monthly income on housing; meanwhile, 27.7 percent, or 342,400 renters, are severely cost burdened, which means they devote more than 50 percent of their income to housing – a significant obstacle for homebuying. Here is a graph on those percentages:

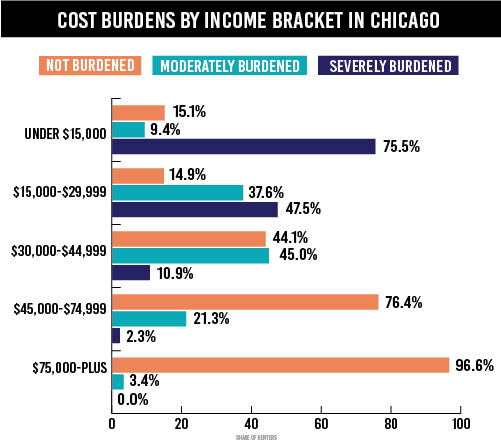

Low-income renters are hit the hardest. According to the Joint Center, for Chicagoland renters earning less than $15,000, 75.5 percent are severely burdened, as are 47.5 percent of renters earning between $15,000 and $29,999. By contrast, for those earning between $45,000 and $74,999, 21.3 percent are moderately burdened, and only 2.3 percent are severely burdened; among those earning more than $75,000, only 3.4 percent are moderately burdened, and none are severely burdened.

Here is a graph on that divide:

A Nationwide Housing Struggle

Chicagoland is not alone in the struggle for affordability. The rental affordability crisis, Harvard’s report made clear, is the result of a perfect storm in housing: the post-boom foreclosure glut drove millions of additional consumers to rent. In the last 10 years, the renting population has spiked by nine million, growing from 34 million in 2005 to nearly 43 million in 2015. Thirty-seven percent of all U.S. households now rent, the highest share since the mid-1960s, and the Joint Center predicts that, with current growth trends, renter households will increase by another 4.4 million by 2025.

Those millions of new renters have driven a surge in demand, pushing rents to historic highs while wage growth has stalled. While median renter housing costs have risen 7 percent since 2001, the median renter income has fallen 9 percent, compounding the difficulty for America’s renters to save up for a home.

Who is Renting?

Even though the majority of renters are at the lowest income level, renting has grown the most among the highest earners, rising 61 percent from 2005 to 2015. Harvard found that 18 percent of renters have incomes of $100,000 or higher, while 38 percent have incomes between $25,000 and $99,999, and 45 percent make less than $25,000.

Renting has risen most in the 50 and older crowd, where renter households grew 55 percent (compared to 34 percent for Gen Xers and 11 percent for Millennials). The number of 50-plus renters grew 50 percent, from 10 million to 15 million.

Not Enough Rentals

For the first nine months of 2015, multifamily construction operated at a rate of 401,000 units, which is higher than any point since the 1980s and 3.5 times the 108,900 units of 2009. Despite that rise in construction, the units hitting the market tend to be more expensive. In 2014, the median rent for new units was $1,372, compared to the $934 for the overall rental stock.

The current rate of new construction hasn’t kept pace with rental demand. Nine million renters have entered the housing market in the last 10 years, and in 2015’s first three quarters, the national vacancy rate was just 7.1 percent, its lowest point in 30 years. As of 2013, there were only 7.2 million units of affordable housing for 11.1 million low-income renters, or 34 rentals to every 100 renters. In large counties of 500,000 or more people, the problem was more pronounced, with 25 affordable units to every 100 renters.

Homebuying Chokehold

All those trends – soaring demand, stagnant or falling wages, insufficient supply of affordable housing – have contributed to the affordability crisis in rental housing, which does not, contrary to conventional wisdom, bode well for the future of homebuying.

Some may argue that historically low interest rates and historically high rents will drive demand for the financial advantage of owning; the homeownership rate will increase, renting will return to its historic levels and housing will finally recover from its post-boom blues.

Recent research contradicts that line of reasoning. According to a study Freddie Mac conducted of renters who have seen their housing costs rise in the last year, 70 percent stated that they could not afford to purchase a home, and 51 percent stated that they have no plans to buy a home. The reason is simple: because renters are devoting more and more of their incomes to housing, they are unable to adequately save for downpayments. New research from The Pew Trust found that one in three American households has no savings, while 25 percent have less than $400 in savings. Even when Fannie Mae (in an explicit push to increase homeownership) lowered its guarantee threshold in 2014 to include mortgages with 3 percent down payments, the results were negligible – for mortgages with LTVs of 95 percent or greater, Fannie Mae comprised just 2.29 percent or the market in 2015, according to research from Black Knight.