Student loan debt may be an even bigger problem than we initially thought.

Here’s an eye-opening statistic – 31.5 percent of Americans who are paying down their student debt are at least a month behind on their payments.

That insight came courtesy of new research from the Federal Reserve Bank of St. Louis, which took a fresh look at student debt and walked away with some alarming conclusions.

A Matter of Perspective

As The Wall Street Journal explained in an overview of the findings, what the Fed essentially did was take a more specific look at the student debt problem. All official measurements of student debt delinquency by the Education Department and the New York Fed take into account all student debt holders, meaning even students who are not required to make payments (for instance, current students or unemployed graduates on grace period).

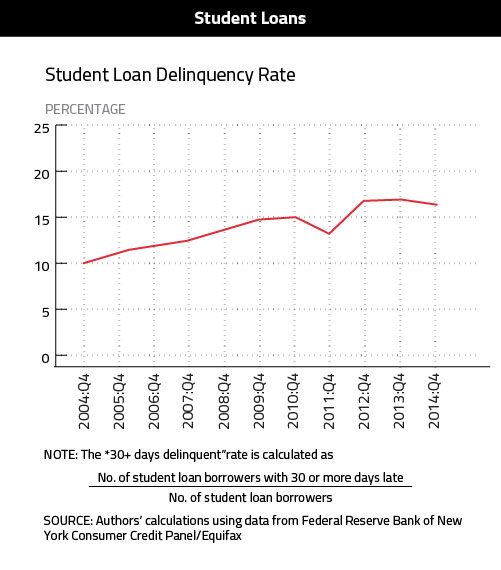

When all those students are considered, here’s what the delinquency picture looks like:

According to those measurements, roughly 17 percent of student debt holders are delinquent – hardly encouraging, but not at the aforementioned levels.

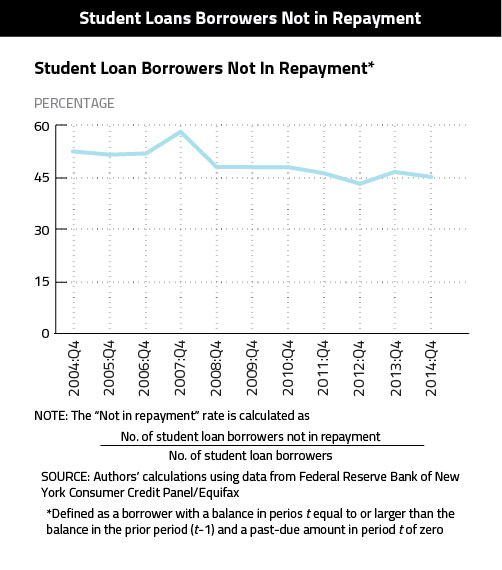

To uncover that 31.5 percent number, the St. Louis Fed only looked at the percentage of student loans that are in repayment, which amounts to 55 percent of borrowers (the other 45 percent, as we just explained, are either current students or on grace period). Here’s how that graph looks:

So finally, when the St. Louis Fed analyzed that 55 percent of student debt borrowers, they arrived at the 31.5 percent delinquency rating, which is dramatically higher than all other forms of consumer credit; consider, for instance, that the delinquency rate for auto loans is just 8.5 percent.

Student Debt and Housing

The Fed does point out in its analysis that delinquencies are not rising, but they’re also not falling; rather, they’re staying at the same elevated level, and that does not spell good news for housing. As we recently reported, complementary studies from the Federal Reserve found that nationwide, 48 states saw a “parental co-residence rate” – essentially, the share of homes with a 25-year-old child living with parents – of between 20 and 30 percent, up from 25 states in 2003; furthermore, in 12 states, that rate is now above 50 percent.

Buying a home is ultimately a financial decision, and student debt is clearly placing a financial strain on Millennials, one that is especially pronounced when combined with stagnant wages and other remnants of the economic downturn.